Your home could be your greatest asset – but not in the way you think

August 30th 2017 | Categories: Home Loans & Leveraging Equity |

Many of us have grown up hearing the old adage “your home is your greatest asset”. For the majority of us it is true that the value of our home does make it one of the most expensive things we own.

Some may not consider the typical family home as an asset – if it’s not generating an income, it isn’t an asset, right? Well this is true to a degree; a true wealth creating asset is something that generates an income, and where the cost of borrowing to purchase (i.e. interest expenses) are tax deductible. The regular family home doesn’t generate an income, and the interest on your mortgage is not tax deductible.

But does this mean your home cannot be an asset? No.

Could your home be your greatest asset? Get in touch to find out.

[ninja_form id=41]

For most, your home will appreciate in value over time such that the capital growth contributes to our net worth. And there is a way that you can transform your mortgage from bad debt into good debt; making it tax deductible.

So how can we leverage the ‘investment’ we make in our homes to help us with our retirement goals?

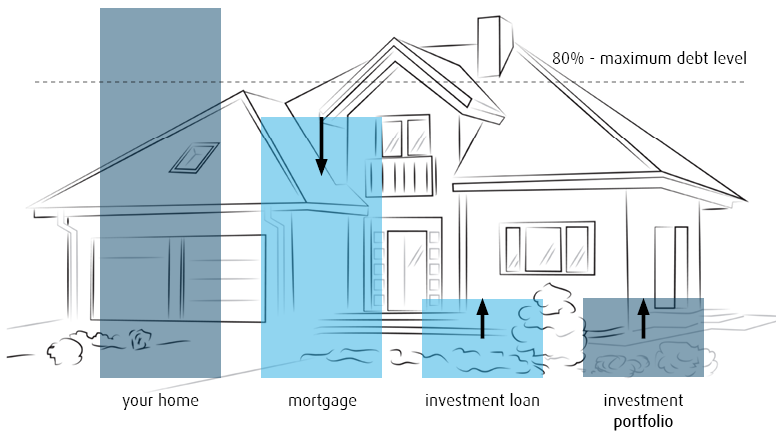

If you have more than 80% equity in your home, that is to say that the value of your home less the outstanding debt on your mortgage is more than 20%, there is potential to use that equity for a greater purpose.

Historically, it was sound advice to pay your home loan off first, then start saving for retirement. With increasing cost of housing paired with longer life spans, this advice isn’t the best for everyone anymore. For many, we need to work harder than that.

If you can answer yes to the following five questions, then the concept of ‘debt recycling’ might work for you. This approach isn’t for everyone; there are a few key considerations to make.

-

Is the current value of your mortgage less than 80% of the value of your home?

-

Do you have time on your side – a long-term investment focus?

-

Do you have a consistent reliable income delivering a surplus beyond your living expenses and interest repayment obligations?

-

Are you comfortable holding debt?

-

Do you have the discipline and tolerance to invest consistently over time?

If you answered yes to all of the above, then the concept of ‘debt recycling’ might work for you. It is very important that you work with an adviser to flush out your own individual circumstances and variables to ensure the strategy is a good fit.

The number one friend of investing is time. The longer you have funds invested, the greater chance of creating growth.

Debt recycling is a financial strategy that allows you to leverage the idle equity in your home and use those funds to invest in an income producing asset like an investment fund, shares or investment property. You can then use the income from the investment, along with any tax advantages from the geared investment, to reduce the non-deductible debt in your home loan.

It means you start saving for retirement much earlier than if you had waited until your home loan was completely paid off.

[bs_button size=”block” type=”link” value=”Download our free introductory guide to debt recycling” href=”http://www.investblue.com.au/debt-recycling/introductory-guide/lp”]

If you would like one of our advisers to get in touch to discuss, complete the form below.

[ninja_form id=41]

This strategy is not suitable for all people and is best implemented under the advice and guidance of a professional financial adviser.

What you need to know

This information is provided by Invest Blue Pty Ltd (ABN 91 100 874 744). The information contained in this article is of general nature only and does not take into account the objectives, financial situation or needs of any particular person. Therefore, before making any decision, you should consider the appropriateness of the advice with regards to those matters and seek personal financial, tax and/or legal advice prior to acting on this information. Read our Financial Services Guide for information about our services, including the fees and other benefits that AMP companies and their representatives may receive in relations to products and services provided to you.

Posted in Home Loans & Leveraging Equity