Spotlight on Personal Loans – trends and ways to repay your loan faster

January 16th 2020 | Categories: Debt Management |

A personal loan is a form of credit provided to you by a lender, such as a bank, credit union or other financial entity such as a peer-to-peer lender. These types of loans are usually taken out to purchase a vehicle, renovate a home, consolidate debt, take a holiday, a special occasion such as a wedding or for education.

Two in five Aussie adults have taken out a personal loan, according to recent research[1]. Used for the right purposes, personal loans can be an effective way of paying for important purchases or study. Paying them off however can be a challenge. Here we look at personal loan repayments and ways to pay them off sooner.

Understand how a financial adviser can support you with your need for financial security. Get in touch.

[ninja_form id=37]

How much can you borrow and for what purpose?

The amount that can be borrowed under a personal loan varies and the need for a personal loan needs to be well-thought through, as the failure to repay these loans can result in a significant amount of debt and a bad credit rating. One site claims ‘A Personalised Loan for Almost Any Need’, that can be between $5,000 and $50,000[2], and while it’s not easy to be approved for a loan that you cannot show to be able to repay, it is strongly encouraged that you first think about whether there is another way to finance your need, and how much is it you really need.

On the flip side, a personal loan may be the best and most affordable way to pay for something important, e.g. As reported by sympleloans.com.au:

- Paying off Credit Cards

- Consolidating debt

- Buying a vehicle

- Booking a holiday

- Paying for a wedding

- Renovating your home

- Education expenses

- Medical costs

The interest rates vary greatly for personal loans and are based primarily on whether you have an asset to secure the loan. This is the difference between a secured and unsecured personal loan.

When we completed our repayments case study further on in this article, using a quick search we saw interest rates (using NSW as the location) vary from 4.69% pa to 20.25% pa[3], so interest rates can vary greatly.

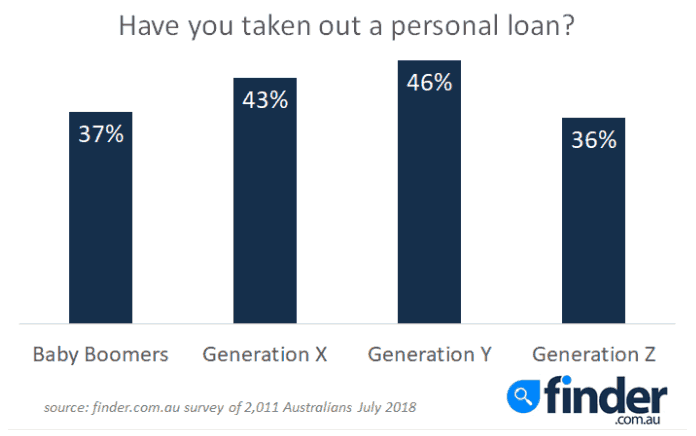

Personal loans by generation – a snapshot

Findings from a finder.com.au survey of over 2,000 Australian Adults reports that the generation relying the most on personal loans is Millennials, with almost half (46%) taking out personal loans. These loans are being taken out primarily for cars (19%)[4]. Overall, the percentage across all generations for taking out personal loans is still high.

Figure 1: Percentage of Australians who have taken out personal loans by generation

Of those reported to be taking out personal loans, most were for planned purchases such as cars, holidays, renovations, education and special occasions like weddings. Thought should be given to what kind of personal loan, and how much, is appropriate for any individual.

Loan repayments and the advantages of paying off sooner

If you have a personal loan, you will want to pay it off ASAP! What are the best options to do this?

One option is to pay your loan off faster. This will not only save you interest but will give you additional cashflow once the loan is paid off.

Let’s take the lowest fixed interest rate loan we found on website Mozo.com.au, a site that compares lenders including banks, peer to peer lenders and non-bank lenders and compares loans based on your borrowing needs. As at 9th January 2020, the site had 226 personal loans on offer to compare[5].

It’s always important to bear in mind that the longer you take to pay back a loan, the more interest you will pay. Put another way, the sooner you pay back the loan, the more interest you will save and additionally the more cashflow you will have.

The lowest interest loan on the day was the Harmoney Unsecured Personal Loan against the loan amount we selected of $30,000. At 6.99% pa, the monthly repayments were $594 and the total cost of the loan $35,640 excluding fees and charges.

By adding additional repayments (in this case monthly) of $20, $50 or $100 per week, the Harmoney Unsecured Personal Loan can be paid off sooner, saving interest and increasing cashflow.

Table 1: Harmoney Unsecured Personal Loan Possible Savings*

| Pay off in 5 Years $594pm | Add an extra $20pw | Add an extra $50pw | Add an extra $100pw | Interest Rate | |

| Monthly repayment | $594 | $674 | $794 | $994 | 6.99% pa |

| Month loan is paid off (1-60) | 60 | 52 | 43 | 34 | |

| Interest saved | $0 | $824 | $1,714 | $2,542 | |

| Additional cash-flow to month 60 (the original loan repayment timeframe) | $0 | $5,392 | $13,498 | $25,844 |

*Based on a five-year (60 month) repayment schedule. Figures are approximate only. Figures exclude fees and charges.

*Please note that this data is not complete and has been taken directly from the source on the date below. The source should be consulted for all data, not this report. Source: https://mozo.com.au/personal-loans, 9th January 2020.

Using the above example, we can see that even an additional $20 per week will save you $824 in interest and generate an extra $5,392 in cashflow to month 60 assuming you continue setting aside $674 per month once you’ve paid off the loan ($674 per month you’re saving x 8 months).

Biting the bullet and paying an additional $100 per week will save you $2,542 in interest and give you an additional $25,844 in cashflow to month 60 assuming you continue setting aside $994 per month once you’ve paid off the loan ($994 per month you’re saving x 26 months). That’s nearly $12,000 per year.

Paying off your loan sooner or on time should also positively impact your credit rating, and if you really need to, can give you options to re-draw credit.

Other options you can consider for paying off your loan faster is looking at consolidating your existing debt, or utilising any available credit on existing loans, in particular, a home loan.

How financial advice helps with debt consolidation and personal loans

A financial adviser will firstly be able to help you map out your goals, and help you to identify what it is that is truly important to you. This will help you budget for how to achieve your goals and dreams.

When it comes to paying off or consolidating debt, your adviser can help you to determine the best way to approach your debt for your situation. They may recommend looking at your existing mortgage for redraw potential or identifying a new loan to roll your existing loans into that offers a better deal. As you can see below however understanding and managing debt is more than simply identifying the right loan. A financial adviser will be able to help you from the beginning of understanding your debt to the daily management of your cashflow.

When Clients come to us with existing debt, we first like to understand what the debt has been used for in order classify what is ‘good debt’ (tax-deductible) and what is ‘bad debt’ (non-tax-deductible). We then look at how we can tackle the debt, ideally looking at options relating to reducing bad debt, starting with the largest debt at the highest interest rate. We can consider payment strategies, budget reviews, redraw options, consolidation, and/or low-interest loans as potential solutions. Overall, the acknowledgment of debt, followed by wanting to proactively reduce it is the most important first steps. We want to work with our clients to identify what they can do each day to make a positive impact on paying off their debt faster.

Invest Blue Financial Adviser.

Invest Blue has a cross-functional team to support your financial needs. We have Advisers to help with your entire financial outlook, as well as a specialised Lending Team. We also have a debt and lending philosophy you can check out here.

Reach out to Invest Blue today for personalised credit advice that respects your complete financial plan.

[ninja_form id=41]

Join our Money Bounceback Challenge! If you want to save $1,000 in 10 weeks, look no further! Join our Money Bounce Back Challenge and refer a friend to get your savings started this year! Join here.

[1] https://www.finder.com.au/press-release-oct-2018-46-of-millennials-turn-to-personal-loans

[2] https://www.sympleloans.com.au/personal-loans

[3] https://mozo.com.au/personal-loans

[4] https://www.finder.com.au/press-release-oct-2018-46-of-millennials-turn-to-personal-loans

[5] https://mozo.com.au/personal-loans.

What you need to know

This information is provided by Invest Blue Pty Ltd (ABN 91 100 874 744). The information contained in this article is of general nature only and does not take into account the objectives, financial situation or needs of any particular person. Therefore, before making any decision, you should consider the appropriateness of the advice with regards to those matters and seek personal financial, tax and/or legal advice prior to acting on this information. Read our Financial Services Guide for information about our services, including the fees and other benefits that AMP companies and their representatives may receive in relations to products and services provided to you.

Posted in Debt Management