Boosting Your Super After Accessing 10k Withdrawal

September 3rd 2020 | Categories: Superannuation & SMSF |

Impact of Dip or Early Withdrawal

Over 1.8 million Australians have withdrawn a total of $13.5 billion from their super accounts to support them during these uncertain times. The early withdrawal scheme was available for those financially impacted by COVID-19 giving them the ability to access up to $10,000 in the 19-20 financial year and an additional $10,000 in the 20-21 year. While this scheme has been crucial for many households to ride out these difficult times, it’s also just as important to consider your options for boosting your super into the future once you have financially recovered.

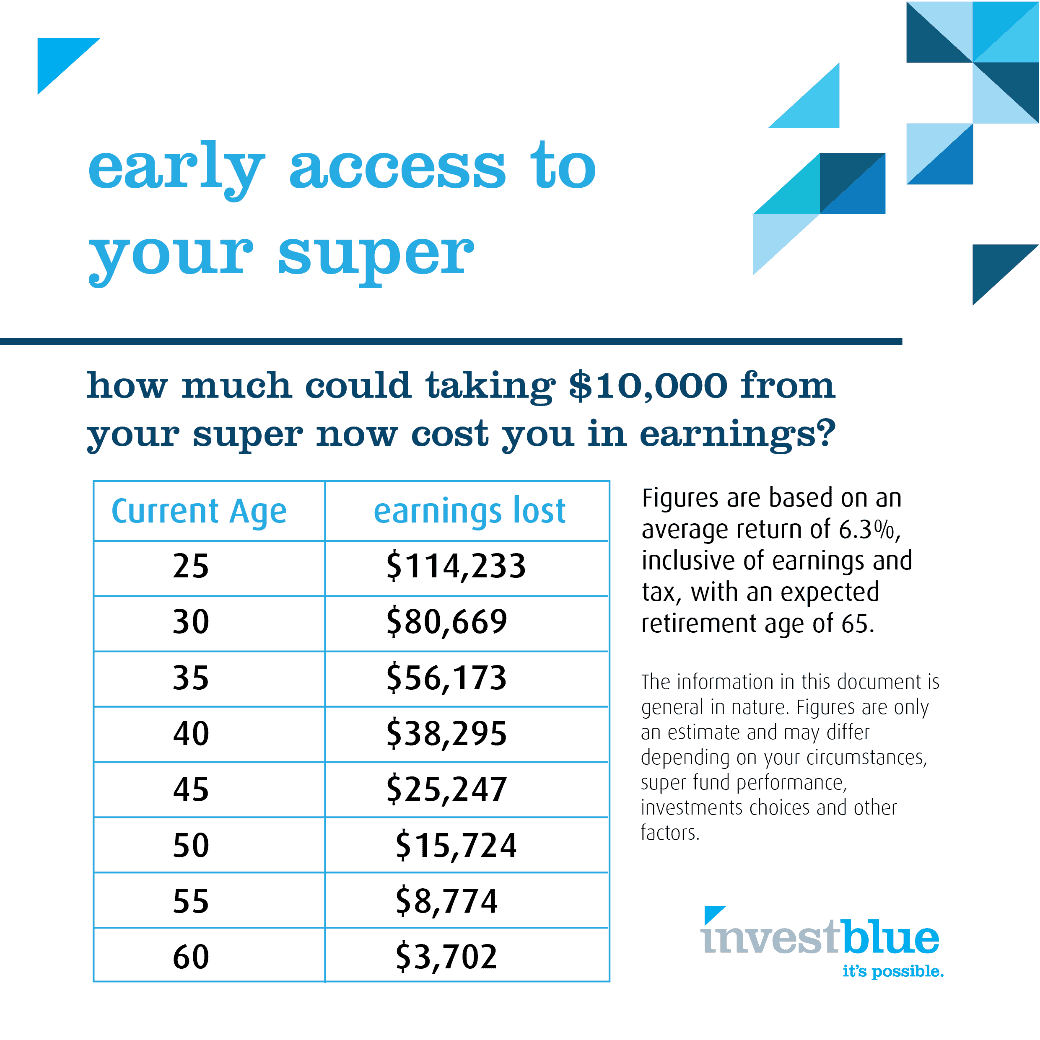

The premise of superannuation fund works on the power of compounding. The higher your super balance, the higher the earnings and investment growth. An early withdrawal from your super can therefore result in a loss of potential earnings from compounding growth in the long term. The potential earnings lost depend on your current age and a number of other factors.

For instance, if you are 25 years old today and withdraw $10,000 from your super account, you will be down the $10,000 plus the potential earnings on the compounding growth which on average would be $114,233 by the time you retire. However, if you are closer to the retirement age, say at 60 years of age, the loss of earnings is estimated at $3,702 on top the $10,000 that you withdraw early as shown below.

You may be interested in our articles:

Should I take money out of my super fund early

How much do you need for a comfortable retirement

Are you looking towards the future however aren’t sure how to finance it? Talk to us today about how to structure a financial plan that starts with your dreams and goals.

[ninja_form id=37]

How to Recover Your Super

Accessing the early withdrawal may serve to meet your current financial needs and requirements but will impact the funds available and financial position post-retirement. It is recommended to review your super and strategise ways to boost your super after a dip or $10K withdrawal. Below we discuss some of these options:

- Make additional Contributions: The economic conditions are not yet back to normal. Therefore, replacing the complete $10,000 may not be a feasible alternative for many. It is; however, possible to make small and regular contributions to the super account to make up for the withdrawal. You may choose to make small recurring repayment or make lump-sum payments when you receive payments such as tax returns or bonuses. According to QSuper if you wish to boost up the dip in five years, you need to make an additional contribution of $45 per week and recovery in ten years will require an additional contribution of $26 per week.

- Salary Sacrificing: Another possible method to boost up your super after an early withdrawal is to increase voluntary contributions through salary sacrificing. Salary sacrificing is an efficient way of boosting up the super account as it is tax-effective, taxed at the rate of 15%, compared to the standard income tax rate of up to 45%. Your payroll officer will be able to assist you in setting up salary sacrificing.

- Topping Up Super After Retirement Through Downsizing: Downsizing is another way to contribute to your super account. Individuals who have already reached the age of 65 and are selling their family home of more than ten years can contribute an additional $300,000 to their super fund from the sales proceeds. These downsizing contributions are beyond the concessional and non-concessional caps on super contributions and are an excellent means to recover lost income and early withdrawals.

- Review your super fund portfolio: For many you may not have reviewed your super or ever considered where your super is how it is invested. Now could be a great time to put in the effort to review the structure, performance and fees associated with your super. Most super has levels of insurance such TPD insurance built into it. It’s a good idea to make yourself familiar with the benefits built into your super and also ensure you’re not doubling up on payments on insurance inside and potentially outside of your super. You may choose to seek the advice of a financial planner to find out which super is best for you, ensure you aren’t paying too much in fees and that your portfolio is invested in accordance to your life stage, risk tolerance and personal goals.

- Rethink the Second Withdrawal: The government program also includes a provision to withdraw a second $10,000 after the end of the financial year on June 30, 2020. Industry Super Australia received 511,000 applications for the early withdrawal of super in the week between June 29 and July 3, 2020. Of the received applications, 346,000 were for the second withdrawal. It indicates that people are withdrawing the maximum limit available to them and could end up in trouble down the track. It is recommended to consider well before taking the additional $10,000 because by taking more money out, it will become all the harder to boost up your super balance later. Your retirement nest could suffer an irrecoverable loss.

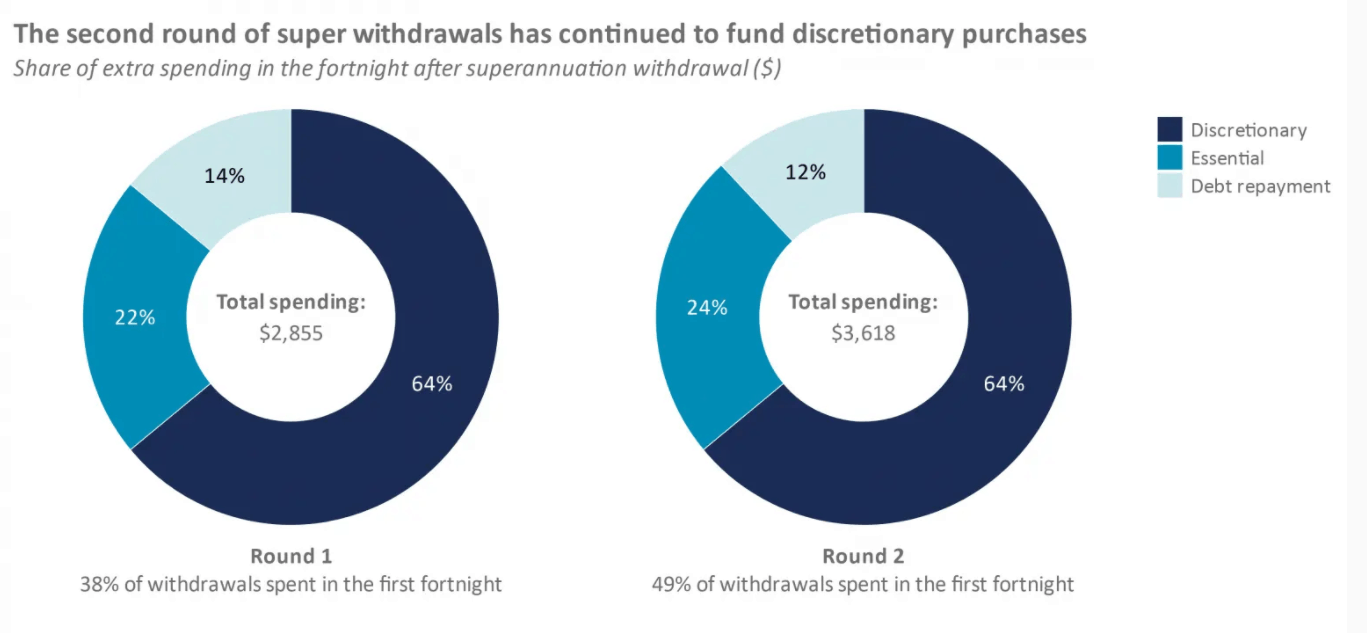

It is important to use your super withdrawals wisely and ensure you are only accessing it if you need to spend it where you need to. Analysts reveal 40% of those accessing their super had no drop in income during the pandemic and a there was a whopping 64% increase on spending towards non-essentials compared to the 14% increase spent on debt repayments.

It is important to keep in mind your super is an asset and grows in compounding interest. It’s also important not to lose sight of long-term goals such as your retirement savings to ensure you can live your best possible life in retirement.

You may also be interested in our articles:

- Is it too late to grow my super

- Can you do more with your super

- Prepping your nest egg for retirement

The government’s initiative to allow people to withdraw early from their super fund to meet their short-term needs during the current crisis is a much-needed step. It can help you to stay on top of your bills and repayments during the ongoing financially difficult times. Additionally, the withdrawal is tax-free, and the unused amount can be added back later as a voluntary contribution.

If you are concerned about the balance of your super or want to discuss which strategy to boost your super is right for you, or to simply review your super, one of our advisers will be able to assist you.

Book your complimentary initial consultation with one of our advisers today.

[ninja_form id=41]

What you need to know

This information is provided by Invest Blue Pty Ltd (ABN 91 100 874 744). The information contained in this article is of general nature only and does not take into account the objectives, financial situation or needs of any particular person. Therefore, before making any decision, you should consider the appropriateness of the advice with regards to those matters and seek personal financial, tax and/or legal advice prior to acting on this information. Read our Financial Services Guide for information about our services, including the fees and other benefits that AMP companies and their representatives may receive in relations to products and services provided to you.

Posted in Superannuation & SMSF